The Complete Guide to Due Diligence

3 Feb 2026A useful guide for anyone considering buying or selling a business in the UK. This article was written collaboratively by Neil Nichols, Founder of Accounts and Legal, and Rachel Duncan, Legal Director at Accounts and Legal.

Due Diligence (DD) is often overlooked by many entrepreneurs, but it’s fundamental to the process of buying or selling a business. Think of it as being like getting a survey on a house before it goes on sale. DD is designed to assess the risk factors for both the buyer and seller from a financial and legal perspective. Without a thorough understanding of the business in question, a buyer may purchase something with unknown problems lurking beneath the surface. DD, done properly, identifies the risks beforehand, making both parties aware so they can make an informed decision.

This list has been compiled using our combined experience of over 50 years in the industry, and is aimed at buyers, sellers, investors and anyone else preparing to acquire or sell a small or medium-sized business.

So, without further ado, let’s start with the basics:

What is Due Diligence?

In simple terms, DD is the process of reviewing relevant financial elements of a business before sale to uncover potential risks or problems that might tbe in place or occur in the future. It’s not necessarily a negative. It’s a chance to prove the business is financially sound, legally compliant and operationally viable in the long term. The areas which due diligence covers are:

- Financial Due Diligence – this takes a thorough look into the numbers, revenue, margins, EBITDA, working capital, cashflow and more.

- Legal Due Diligence – a review of all of a business’s contracts, liabilities, intellectual property, employee handbook and HR documents, corporate structure, shareholdings and more.

- Tax Due Diligence – reviews any issues with HMRC, compliance with VAT, PAYE, any R&D claims and any other ongoing enquiries.

- Operational Due Diligence – this looks into how the business operates, asking questions such as, what are the systems and processes like? Does the technology or machinery need updating? Are the staff effective? How reliable is the business?

- Commercial Due Diligence – this takes a further look into the wider market conditions, along with things like customer or client retention, any major competition and any strategic risks to the business.

As you can probably tell, it’s an incredibly thorough look under the bonnet of a business. Buying or selling a business is a huge financial move, so both parties need to have full confidence, which can only be attained by having all the information at your disposal.

A Quick Note Before We Dive in

This article applies to both an asset or share purchase, which are very different and mean different things for buyers and sellers.

A Share Purchase is where you acquire the entire company, including all its liabilities

An Asset Purchase, however, is where you buy selected assets often without inheriting the risks associated with them.

This is very much a topline summary, and the main thing to be aware of is that the tax implications vary widely between the two purchase types. It’s something we see lots of business owners get confused about, so if you’re still unsure about what type of purchase you’re going to undertake, we’d suggest reading this article first:

Asset vs Share Sale: Understanding Tax When Selling a Business

Financial Due Diligence: Get to Know the Numbers

Financial DD goes way beyond analysing a business’s accounts, it’s about understanding the financial reality underpinning operations and assessing whether the valuation you’ve agreed is justified.

Revenue and EBITDA

Revenue is the core of any valuation; however, it can’t always be taken at face value. For that reason, EBITDA (earnings before interest, taxes, depreciation and amortisation) is often used as the basis for valuations to avoid sellers clouding the truth or presenting the best version of their business with misleading figures. Using EBITDA, it’s valuations might be adjusted for:

- One-off costs or exceptional income

- Non-commercial expenses run through the business

- Owner’s salary if it is above or below market rate

- Costs that will not continue post-sale

- Sudden growth that’s not backed by contracts

How are these things checked? By cross-referencing the figure against what is displayed in any:

- Management Accounts

- Bank statements

- VAT Returns

- Customer and supplier contracts

- Cashflow forecasts

- Outstanding Debtors

Fundamentally, you’re looking for consistency and stability when it comes to revenue. Spikes from one-off work might look great on paper, but they may not be reliable or predictable.

Understand Working Capital Requirements

Working Capital is one of the biggest reasons why deals fall through or end up being re-negotiated. In simple terms, working capital is the day-to-day cash amount that a business needs to operate. It includes all the money tied up in stock, invoices waiting to be paid, and bills becoming due.

Example:

If a business has £50,000 of customer invoices waiting to be paid, £30,000 of stock, and £40,000 of upcoming bills, its working capital position is:

£50,000 + £30,000 – £40,000 = £40,000.

That £40,000 is what keeps the business moving, buying materials, paying staff, fulfilling orders. If the business doesn’t have enough working capital, even a profitable company can quickly run into cashflow problems.

If a business doesn’t have enough working capital, it can appear profitable on paper while struggling to pay suppliers or pay staff in real life. As a buyer, you need to know whether the business creates enough working capital to operate day-to-day, and whether that working capital fluctuates during the year.

The key checks to identify working capital include:

- Debtor days: how long it takes customers/clients to pay on average

- How quickly suppliers must be paid

- Stock levels; how quickly they diminish/need to be replaced

- Any seasonal cash needs or fluctuations

- Whether the business is stretching creditors to survive

A lot of buyers might underestimate the cash needed to run the business. A good working capital review presents any nasty surprises and ensures you understand the true cash demands from the get-go.

Read More: Buying a Business: The Complete Guide to a Successful Purchase

Analyse Profitability and Margins

As mentioned, revenue can be deceiving. A business may show a healthy top line, but unstable or declining margins can be indicative of a deeper truth. Revenue tells you how much a business sells, but margins tell you how efficiently it operates, how well it prices and overall, how resilient the business is to cost pressure. In a lot of instances, margins can provide a far more accurate picture of long-term sustainability than headline profit figures.

Start by examining your gross margins, (profit after deducting cost of goods) ideally broken down by product, service or customer group. By doing this, you’ll gain a greater understanding of which parts of he business are not optimal. A business with great revenue but poor margins may have a problem with under-pricing, or perhaps overspending, or is maybe struggling with waste, or inefficiencies.

On the other side, a business with a highly variable gross profit margin may be overly reliant on one-off work which can’t always be relied on or replicated post-acquisition.

For this reason, margin consistency over the last three to five years is a good indicator for potential buyers. Stable or improving margins point to a reliable, well-run business. Declining margins may show competitive pressures, operational problems or a business struggling to stay afloat. Consistency is key, and a buyer will want to know they can step into the driving seat with a reliable source of income.

Margins often tell you more about a business than any other financial metric. They uncover how well a business is currently running, and also how well it will do in the future. For buyers, they’re incredibly important as they demonstrate where the business is at and how resilient the business truly is.

Examine Assets, Liabilities and Debts

Not every liability will be visible. Although some will clearly be disclosed in the balance sheet, others may be buried in contracts, finance agreements or historic decisions. A thorough DD process will start by reviewing the business’s assets and whether they’ve been valued correctly. This includes tangible assets like machinery, vehicles, equipment, fixtures and fittings as well as intangible assets like software, intellectual property, licenses and goodwill. Any assets that are recorded at a historic cost may no longer be worth the same amount which will not only affect the valuation but will mean the potential buyer may have to account for replacing those assets in the future.

Next, we’ll examine the lease and finance agreements, including property and equipment leases, vehicle and finance arrangements, break clauses, rent reviews or restrictions in assignment. In most cases these agreements will continue after the sale, so it’s important the buyer knows their future obligations under these agreements and whether there’s any flexibility in the terms in case they want to negotiate or cancel any of the agreements post-acquisition.

Crucially, sellers do not always distinguish clearly between liabilities that will remain with them and those that will pass to the buyer, particularly in less formal SME transactions. Some obligations may be assumed to “sit with the company” without explicit discussion. Your DD process must identify all liabilities, clarify who is responsible for them post-completion, and ensure they are reflected appropriately in the purchase price, warranties or indemnities.

The DD process doesn’t just protect you from unexpected costs, it also strengthens your negotiating position, which may help you renegotiate the purchase price.

Case Study: How We Helped Westland Asset Successfully Buy a Business

Why Tax Matters During Due Diligence (Asset vs Share Purchase)

Often underestimated during the due diligence process, tax can pose a risk to buyers if not assessed correctly. The key distinction is between an asset and a share purchase. With a share purchase, you’re buying the company itself and everything it encompasses, including its historic tax position. Any tax liabilities that are hidden away will become the responsibility of the new owner. A share purchase is sometimes more commercially simplistic and offers greater continuity, but it does come at the cost of potentially inheriting a historic tax risk.

With an asset purchase, you acquire specific assets and generally any historic tax liabilities are left behind with the seller. An asset sale still comes with tax considerations, though, so it’s not completely risk-free. An asset purchase can ring-fence liabilities but may involve higher upfront tax costs, VAT complexity and operational disruption. The difference between the two types of sale can dramatically change your tax burden, so it’s important to know the difference from day one. With proper tax due diligence you can:

- Understand which risks you are inheriting

- Structure the deal appropriately

- Negotiate any warranties, indemnities or price adjustments

- Avoid unexpected tax liabilities after completion

- Make an informed decision about whether to go ahead.

If you’re weighing up the two options, our due diligence team can help you understand the tax implications and ensure there are no nasty surprises once the deal completes.

Legal Due Diligence: Understanding What You’re Really Buying

Legal due diligence makes sure the business you’re buying is structurally sound, legally compliant and actually owned by the people who are claiming to be selling it. It also protects you from taking on any disputes, obligations or liabilities that could adversely affect your purchase. Below are some of the elements explored during the legal due diligence process:

Structure and Ownership

This confirms that:

- The company exists in the form the seller claims

- Shares are owned by the people selling them

- There aren’t any outstanding charges or security over assets

- Companies House filings are accurate and up to date.

You’d be surprised how many times buyers discover issues with voting rights, historic share transfers or missing statutory records.

Often, when people set up businesses, naturally, they want to save money. There are lots of businesses online that offer cheap incorporation services. In the past, we have seen examples where business owners have used these services, but only when they reached the point of sale did they realise that they didn’t actually own the company. The service they used registered the business in its own name, not the owners’, which later required a lengthy and complex legal transfer of ownership.

Reviewing Key Contracts

Contracts are the foundation of a business, so before you buy, you need to ensure that they’re fit for purpose and do an adequate job of securing the business’s interests. What do we mean by that? Check whether:

- Customer contracts can be transferred

- If key agreements contain change-of-control clauses

- How easy it is for customers to cancel

- Whether suppliers can change pricing after the sale

- Any long-term obligations or exclusivity agreements

A business that’s built on unwritten agreements or handshakes is already on unstable ground. We’ve seen incidents where business owners have serviced clients for years without ever thinking about contracts or cancellation clauses. The reality is, if you don’t have any contracts in place, if your clients all decided to end things, your business instantly falls apart. It might feel unlikely, but a potential buyer will want to make sure this can’t happen. With a proper contract that accounts for notice periods, you have a certain amount of time to replace the client should that day ever come. It may sound obvious, but to a potential buyer, it’s a huge weakness if the business doesn’t have proper contracts. As the saying goes, never build a house on sand.

Case Study: How We Guided Aspire Systems through a UK Business Acquisition

Intellectual Property and Brand

For lots of industries, tech, professional services, e-commerce and more, intellectual property is central to how the business operates. It’s what differentiates a business, and sometimes it’s the reason the business is started. When buying a business, you should ensure that the sellers own their intellectual property and brand. The point of IP is to confirm that the business genuinely owns the intellectual property it relies on, and that those rights are properly protected, transferable and free from dispute. Without this clarity, a buyer risks paying for assets that don’t legally belong to the business at all. So, what counts as intellectual property?

It extends beyond the usual patents and trademarks, it also covers:

- Business and trading names

- Registered and unregistered trademarks

- Domain names and websites

- Software, source code and databases

- Copyright in marketing materials, reports and written content

- Proprietary methodologies, processes and know-how

- Customer data and mailing lists

- Product designs, formulas or technical drawings

If the business can’t operate effectively without it, it should be treated as core intellectual property.

One of the most common problems discovered is that the business doesn’t actually own the IP it uses. This can happen for all kinds of reasons, the most common we’ve seen are:

- Founders created IP before the company was incorporated

- Work was carried out by contractors or freelancers without written IP assignments

- Developers retained ownership of software or code

- Marketing agencies retained rights to branding or creative assets

Intellectual property rarely features in financial statements, and yet they have a disproportionate impact on the value and stability of a business. If you don’t own your IP, it can undermine any competitive advantage you have, lead to expensive disputes, limit future growth and generally cause a big nuisance to business owners. With a thorough look at the IP of a business, before buying or selling, you can ensure any of these problems are ironed out before you go ahead.

Read More: Sell My Business: A Step By Step Guide

HR and Employment Issues

A business’s employees and how they’re transferred after a sale depends on how the deal is structured. In a share purchase, the employing company remains the same, meaning the employees stay in place, and any employment issues also get transferred to the new buyer. TUPE typically does not apply in this case. In an asset purchase, however, employees may transfer under TUPE (the Transfer of Undertakings (Protection of Employment) Regulations), which is designed to protect employees when a business changes hands by preserving their existing terms, rights and continuity of employment.

Regardless of the structure, the HR and Employment side of the business needs to be looked at in fine detail before a business is sold or purchased. Buyers should look at the employment contracts (including any pay or bonus structures), holiday accruals, pension obligations and HR policies, as well as the use of contractors and consultants (a common source of hidden risk if individuals have been misclassified). TUPE can restrict terms or a buyer’s ability to restructure following completion, so it’s something to keep in mind before a purchase.

Regulatory and compliance obligations are easy to overlook but carry some of the most serious risks for business owners. Due diligence will identify what regulations apply to the specific industry, and whether the business holds all the required permissions or licenses to trade lawfully. Data and GDPR compliance will also be assessed to confirm if data is being handled appropriately, and if a business isn’t abiding with data laws, then this could adversely affect the outcome of any potential sale.

Beyond employee contracts and TUPE, there are lots of other areas to be aware of that will become the responsibility of the new owner. Things like any informal arrangements around pay, bonuses or working hours, which if not written down in a contract somewhere, can become a problem. The same goes for HR records, or weak health and safety practices, pension auto-enrolment procedures, what happens with accrued holidays, the list goes on.

In essence, if there is a process around HR or Employment, you need to make sure it’s documented somewhere. The problem we often see is that business owners don’t think about this at the start, and are often left catching up or putting measures in place as their business grows. This may seem fine, but potential buyers need to see documentation and contracts that define these processes. Both so that they can come in and take over seamlessly, and also so they’re protected should anything go wrong.

Commercial & Operational Due Diligence: Does the Business Function?

The legal and financial due diligence gives you a static view of what position the business is in; commercial and operational DD looks at the day-to-day running of the business. Or more importantly, how the business functions and whether it can continue to perform once you take over.

How Strong is the Business’s market position?

Find out where the business sits within its market. Look at its size and scalability in comparison to competitors, assess any barriers to entry, any industry trends or developments that may affect performance in both the long and short term. Are there government regulations coming down the line? Does AI pose a threat? Is there a talent problem in the industry? These are the kind of questions you need to know the answer to before taking the plunge. For example, a profitable business may look incredible on paper, but if it’s operating in a declining or heavily disrupted market, it could be riskier than the numbers suggest. On the other hand, a company with a modest historical performance but a strong position in a growing market may be more attractive to a potential buyer. Ultimately, a buyer will be looking to see if demand is stable, not overly reliant on short-term trends or sensitive to factors that can’t be controlled.

How Reliable and Diversified is the Customer Base?

Having one big client who contributes a huge percentage of revenue may sound good on paper, but it leaves a business vulnerable should the client leave. Often, business owners have cultivated these relationships over years, and don’t even consider the chance they’d leave, but when a new owner comes in, this presents a potential problem. That’s why revenue quality is just as important as quantity. Heavily relying on one or two clients increases risk, particularly when contracts are informal or based on a handshake. Thorough due diligence will analyse the spread of clients, looking at customer retention rates to discover whether the current revenue being reported is recurring or purely one-off.

A business with a good spread of clients paying a recurring fee means regular and predictable revenue, which is ultimately what a new owner wants. Buying a business is difficult and often disruptive, so if the new owner can be confident that they’re stepping into a business that has a broad, stable customer base, it provides reassurance that revenue will continue after completion. This kind of predictability reduces the risk of sudden income drops, supports smoother cashflow management, and allows the buyer to focus on running and growing the business rather than firefighting customer losses.

How Do the Business’s Day-to-Day Operations Actually Work?

Before you buy, you need to know how the business operates in reality. To do that, you need to review internal processes, workflow systems, technology and more, all to help understand whether operations are efficient, repeatable and well documented. This is what the process of operational due diligence will uncover. Any business that relies heavily on manual processes or outdated systems, or has processes that are kept in the heads of employees, may struggle to scale after acquisition. Buyers should identify where processes depend on individuals rather than systems, the purpose being to identify if investment will be needed in these areas post-completion. A buyer will want to understand how the business will run once the deal completes, and if critical processes exist only in people’s heads rather than being properly documented, that dependency can quickly become a concern.

Ultimately, anything that helps a new owner understand how the business operates will reduce risk. Clear customer and supplier contracts, documented processes, system guides, and simple process maps all make a big difference in the early months after completion. They provide continuity, reduce reliance on individual employees, and allow the buyer to step into the business as seamlessly as possible. Businesses that are well documented are not only easier to sell, but also easier to run and scale, which is exactly what most buyers are looking for when they invest in a business.

Is the Business Dependent on the Owner or Key Individuals?

Just like being overly reliant on a few clients, many SMEs are heavily reliant on a few members of staff, often the owner. It’s usually a natural process where the owner becomes the centre of all decisions. We get it, it’s difficult for owners to step away from the business they’ve worked so hard to create. But while this may work day to day, it creates what’s known as a key person risk, the risk that the business can’t run properly without this specific person.

From the perspective of a buyer, this introduces a layer of uncertainty which can sometimes lead to price reductions, tougher deal terms, extended earn-outs or, in some cases, buyers walking away entirely. The way to counteract this is to make the business less reliant on one or a few key individuals well before the sale takes place. How? As mentioned above, documenting key processes helps, along with delegating customer relationships to senior staff, introducing clear reporting lines, and ensuring that operational and commercial decisions are not concentrated in a single role.

Other ways include strengthening the management team, formalising responsibilities and creating continuity through employment contracts or retention incentives, which can all help reassure buyers. Additionally, owners will often agree on a handover period where they support the transition for an agreed time after completion. Businesses that operate without an overreliance on a few key people are not only easier to sell, but they often achieve better outcomes.

Example: The Departure of a Founding Partner at Pret a Manger

An example of this occurred when co-founder of the coffee and sandwich shop chain Pret a Manger, Julian Metcalfe, stepped down from day -to-day operations in 2018. When Julian transitioned out of the business, there was a realisation of just how important Julian’s leadership and brand vision had been to Pret’s growth and identity. Metcalfe’s strengths were deeply embedded in Pret’s culture, store concepts and product development, and his departure triggered a noticeable shift in how suppliers, staff and franchise partners perceived the business. While Pret continued to thrive commercially, the change highlighted the fact that businesses tied closely to the reputation and operational influence of a single individual can experience uncertainty, particularly in leadership transition phases.

Lessons: Pret’s transition demonstrates the importance of planning for life after a founder steps back. Even in a well-run, internationally recognised business, the exit of a key individual can create uncertainty if knowledge, processes and decision-making are too closely tied to one person. Where businesses have clear succession planning, well-documented processes and a capable second-tier management team in place, that transition is far smoother. Addressing key person dependency early not only protects continuity, but also supports valuation and gives buyers confidence that the business can operate successfully under new ownership.

How reliable are the business’s suppliers?

Suppliers are just as important to a business’s continuity as its employees, as supply chain issues can have a direct impact on a business’s margins. Similar to employees, if a business relies heavily on a few suppliers, then it’s opening itself up to risks. Again, it comes back to contracts and documentation. A buyer will want to understand the dependency on certain suppliers, whether those relationships are outlined in contracts, and how easily alternatives could be found if something goes wrong.

Example: The Jaguar Land Rover Cyber Attack

A real-world example of this was in September 2025 when Jaguar Land Rover (JLR) experienced a cyber-attack causing the production of vehicles to stop completely for three weeks. The results were catastrophic, not only for JLR but for the ecosystem of suppliers that relied on their business. Smaller suppliers who provided parts for the larger company faced layoffs and financial strain and were in some cases forced to shut down their operations. The incident demonstrated the ripple effect and fragility of interconnected supplier networks, something that can be a lesson to any business owners looking to sell.

Lessons: Although some events can’t be controlled, some measures can help mitigate the risk:

- Formalise agreements with key suppliers – documented contracts reduce uncertainty about pricing, delivery and continuity.

- Diversify the supplier base so that no single supplier is overly relied on. Supplier diversification massively helps mitigate risk.

- Benchmark costs and alternatives to show that relationships aren’t based solely on personal goodwill.

- Provide documented contingency plans such as back-up suppliers or inventory buffers.

- Share supplier performance and risk assessments with prospective buyers to demonstrate proactive management.

In DD, diverse supplier arrangements not only reduce operational risk but can also preserve the valuation.

Can the business scale and is there potential for growth?

Often, business owners who are selling will say, “this business has great potential.” And while that may well be true, due diligence asks a more practical question: if the potential is genuinely there, why hasn’t it already been realised? Potential on its own isn’t enough. From a buyer’s perspective, value comes not from what could happen, but from what the business has already demonstrated, or from having a clear, credible plan on how to get to the next level.

This is why commercial and operational due diligence focuses closely on whether the business can realistically scale without major disruption or disproportionate investment. A business may be performing well at its current size, but growth may be constrained by limiting factors such as: staff capacity, outdated systems, reliance on the owner, regulatory barriers or a lack of documented processes. In some cases, the business hasn’t grown because it simply couldn’t, not because the owner chose not to.

Understanding these constraints allows buyers to separate genuine growth opportunities from optimistic assumptions. It also helps test whether future returns are achievable within a reasonable timeframe and cost. Businesses that can demonstrate scalable systems, sufficient management depth and a track record of incremental growth tend to inspire far more confidence than those relying solely on untapped “potential” as part of the sale narrative.

What Are the Biggest Commercial Risks to Identify Before Completion?

Taken together, commercial and operational due diligence provides a reality check. It highlights where performance depends on fragile relationships, informal processes or individual knowledge, and where future growth may be constrained by structural issues. For buyers, this insight is invaluable. It informs valuation, strengthens negotiation leverage and helps ensure that the business you’re buying can perform, not just today, but under your ownership.

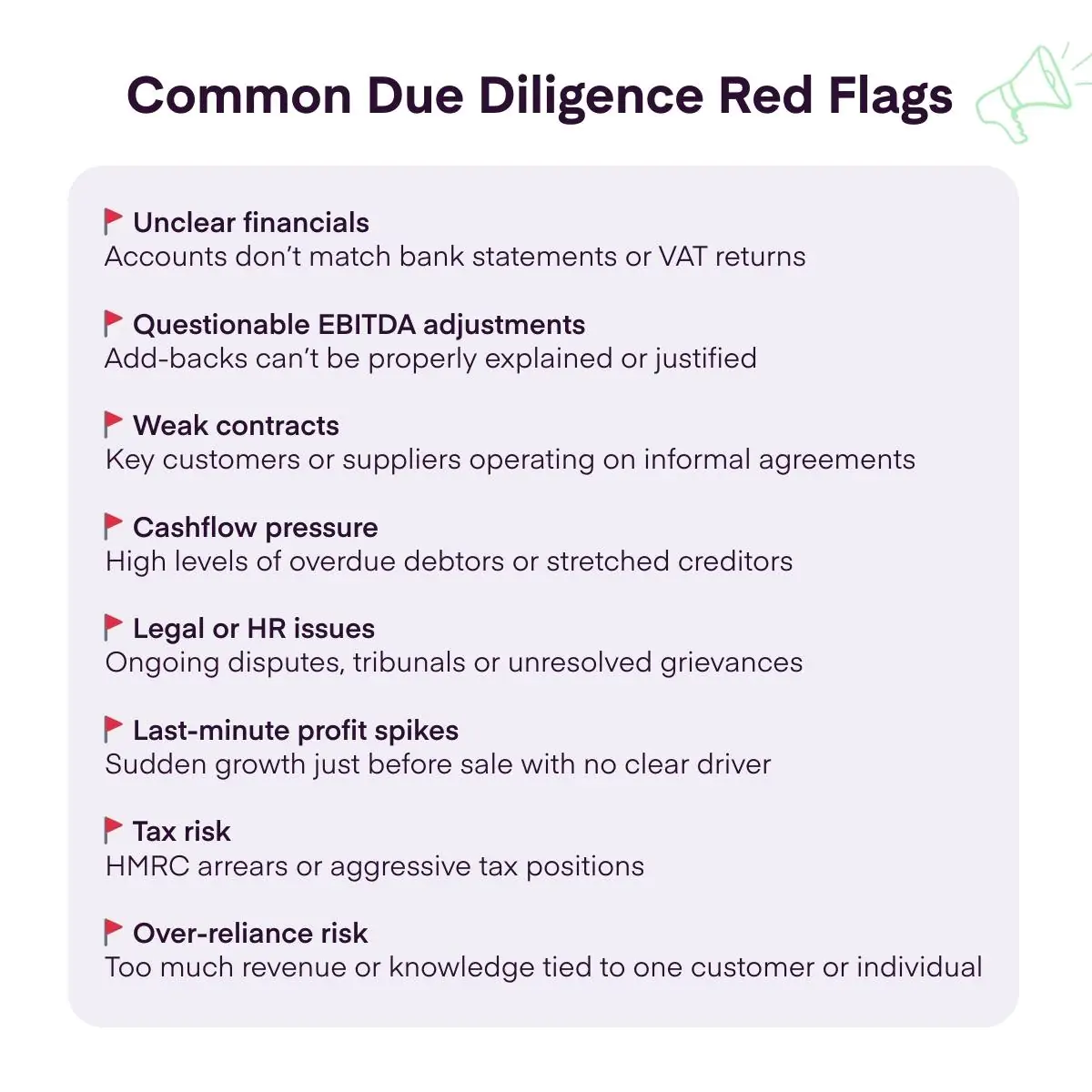

Red Flags to Watch Out For

Some issues uncovered during due diligence aren’t just points for negotiation; they’re warning signs that require serious thought about whether the deal is right at all. It’s our job to uncover these for you as part of the due diligence process, but as an idea, here are just some of the things to look out for.

- Financial statements that don’t match bank records

- EBITDA adjustments that can’t be clearly explained

- Missing or informal customer contracts

- Large amounts of overdue debtor balances

- Ongoing legal disputes or employment tribunal claims

- A sudden spike in profits shortly before the sale

- HMRC arrears or aggressive tax practices

- Heavy reliance on a single customer or key individual

- Over-reliance on a single supplier

Spotting these issues early gives buyers options. In some cases, they justify a price reduction or stronger protections. In others, they may be a sign that walking away is the most commercially sensible decision.

Last Things to Consider about Due Diligence

Buying a business is a decision that should be thought about long and hard. It’s strategic, not a leap of faith, and the role of due diligence isn’t to purposely kill a deal – it’s to ensure you know exactly what you’re buying, what it’s worth and what potential risks may arise.

It’s easy to be blinded by headline figures, optimistic forecasts or the seller’s positive view of the company. But proper due diligence cuts through that, replacing assumptions with facts, highlighting where value is real and exposing weaknesses. In many cases, it doesn’t stop a deal, it simply reshapes it into something more sensible.

Whether you’re a seasoned pro or a first-time buyer, the goal is the same: step into ownership knowing how the business actually works, not how it’s been described.

If you’re in the process of buying a business and want a clear, commercially focused view of the risks and opportunities, our team at Accounts and Legal can support you with financial, legal and tax due diligence, giving you the information you need to make the right decision.

Get in touch if you’d like to find out how we could help your business.