Private Limited Company Advantages & Disadvantages (Updated 2026)

10 Jun 2026This article has been reviewed and updated for the 2026/27 tax year. It reflects current Companies House incorporation fees, mandatory identity verification requirements for directors and people with significant control, and the 2026/27 Corporation Tax and dividend tax rates. As CEO of Accounts and Legal, Neil Ormesher brings over 25 years of expertise in tax planning, accounting, and business strategy. A fully qualified accountant, Neil specialises in helping business owners minimise tax liabilities, optimise business structures, and navigate the complexities of tax-efficient business transactions. Here he talks about advantages and disadvantages of becoming a Private Limited Company:

If you’re thinking of starting or expanding a small business, you have a choice of structures – sole trader, public limited company, business partnership, or private limited company. There is no ‘one-fits-all’ solution for a small business owner so it’s important to assess advantages and disadvantages of each before making a decision on your future business structure.

In this article, we look at private limited company advantages and disadvantages to explain what they offer business owners compared to operating as a sole trader. First, it’s essential to answer the question, ‘what is a private limited company?’.

Not sure whether to stay as a sole trader or set up a limited company? We can compare both options based on your profits, tax position and plans for growth. Book a Discovery Call.

Definition of private limited company

A simple private limited company definition is ‘a company that is a legal entity in its own right, separate from the identity of its owners, and has special status in law’. The assets, liabilities and profits belong to the company, not the owners.

A private limited company is incorporated and registered with Companies House. Most trading businesses use a private company limited by shares, which has shareholders and share capital. Some private companies are limited by guarantee instead, which is more common for not-for-profit or membership organisations.

A private limited company is owned by its shareholders, the people who hold shares in the business. A company can be owned by just one individual who has sole control over all decisions made about the business. Where there are multiple shareholders, each one has voting rights in proportion to the number of shares they hold. If an individual owns or controls more than 25% of the company’s shares or voting rights, they will usually be a person with significant control, or person with significant control (PSC). Someone may also be a PSC if they have the right to appoint or remove a majority of directors, or otherwise exercise significant influence or control over the company.

When should a sole trader consider becoming a limited company?

You may want to review your business structure if your profits are increasing, you are taking on larger contracts, you are hiring staff, you need external funding, or you are concerned about personal liability.

Incorporation can also make sense where you do not need to take all profits out of the business each year, because retained profits can be used for investment, equipment, recruitment or working capital.

However, it should not be treated as an automatic next step. For some sole traders, the tax savings may be limited once accountancy fees and extra administration are taken into account. The decision should be based on your numbers, not a general rule of thumb.Advantages of a private limited company

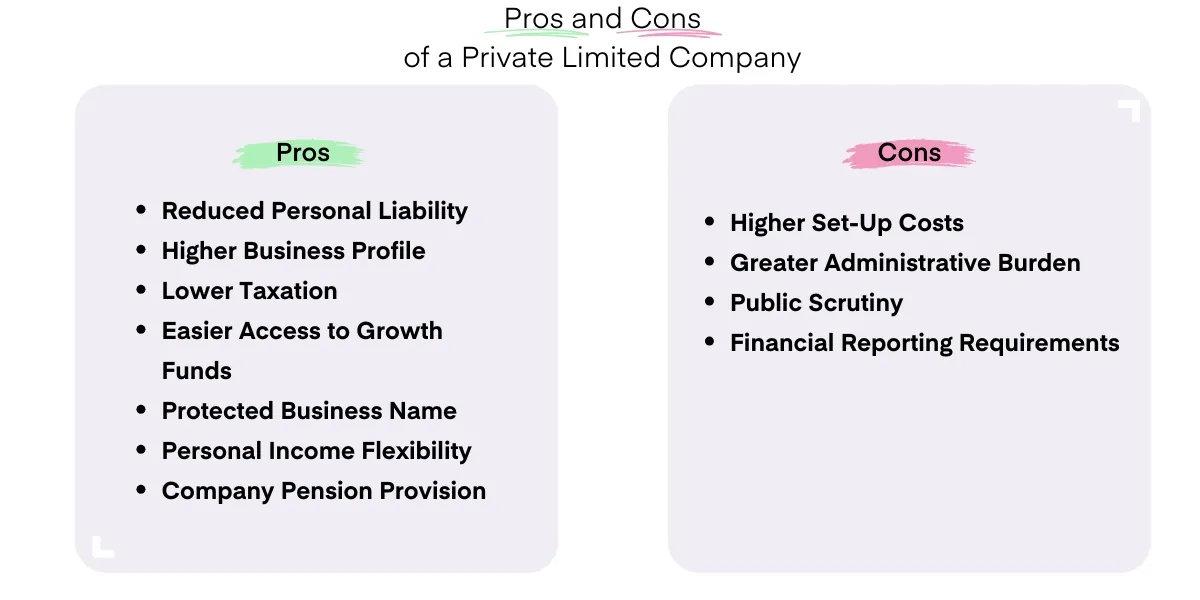

Private limited companies offer a number of important advantages compared to businesses operating as sole traders.

Reduced risk of personal liability

As a sole trader, you are personally liable for all the debts and liabilities of your business. In a company limited by shares, shareholders’ liability is generally limited to any amount unpaid on their shares. However, directors can still face personal exposure in specific circumstances, for example where they have given a personal guarantee, breached their duties, or continued trading improperly when the company was insolvent. That reduces the risk of having your personal assets seized to pay for the debts of the business if it fails.

Related: Everything you need to know about Creditors and Debtors

If you are signing larger contracts, taking on debt or worried about personal exposure, it is worth reviewing whether your current structure gives you enough protection. Book a Discovery Call.

Higher business profile

A private limited company is perceived as more substantial than businesses run by a sole trader. When customers place orders or award contracts, they want to be confident that the supplier has the resources to provide a reliable service. The perception is also shared by investors, so it may be easier to attract funding as a limited company.

Related: What is EIS? - alternative funding options for small businesses

Related: What is SEIS? - Alternative small business funding

Potential Tax Advantages

Sole traders pay income tax and National Insurance contributions on the profits of the business through an annual self-assessment tax return. The rate of income tax and National Insurance contributions is equivalent to that of a private individual and includes the same personal allowances.

A limited company pays Corporation Tax, which is based on income minus allowable business expenditure.

Tax can be one reason to trade through a limited company, but it should not be described as automatically lower. For 2026, Corporation Tax is 19% for companies with profits of £50,000 or less, 25% for profits above £250,000, with marginal relief between those limits. Owner-managers also need to consider tax on salary, dividends and retained profits. A company structure can be more tax-efficient where profits are retained for reinvestment, pension contributions are planned properly, or remuneration is managed carefully, but the best answer depends on profit level, extraction needs and the owner’s wider income.

Although you will also pay personal income tax and National Insurance contributions as a director or owner of a limited company, you have greater flexibility in the way you pay yourself, which can lead to savings on your personal tax bill.

Related: How to pay Corporation Tax: A guide to rates & deadlines

We can compare your current sole trader tax position with a limited company structure and show the likely difference in take-home income. Book a Discovery Call.

Easier access to growth funds

As we mentioned earlier, private limited companies have access to a wider range of funds for growth, including bank loans, venture capital and crowdfunding because investors see limited companies as a lower risk. You can also raise capital by selling shares in your business, although you cannot offer them for public sale.

Related: A guide to crowdfunding and the best crowdfunding sites UK

Protected business name

When you register your business name with Companies House, the name is protected and cannot be used by any other business. Anyone wishing to register a name must check that it is available. If Companies House recognise a matching name or a name that is very similar, they will advise the business and refuse to grant permission. Registering a company name prevents another company from registering the same name, or a name that is too similar under Companies House rules. It does not give the same protection as a registered trade mark and will not, by itself, stop all passing-off or brand infringement risks. Businesses that rely on their brand should also check trade mark availability and consider trade mark registration.

Related: Legal aspects of starting a small business. Don’t make these common mistakes!

Personal income flexibility

If you are an owner or director of a limited private company, you can pay yourself a combination of salary and dividends. Dividends are not subject to employee or employer National Insurance, and dividend tax rates are generally lower than income tax rates. However, dividends are paid from post-Corporation Tax profits and are only available where the company has sufficient distributable profits. For 2026/27, the dividend allowance is £500 and dividend tax rates above the allowance are 10.75% for basic-rate taxpayers, 35.75% for higher-rate taxpayers and 39.35% for additional-rate taxpayers. This means a salary-and-dividend strategy may still be tax-efficient, but it should be calculated rather than assumed.

There are also other ways to take money out of the business as a director, including bonus payments, pension contributions, directors’ loans and private investments. These offer various degrees of tax efficiency. Sole traders do not have the same flexibility. They take income from the profits of the business and the income is taxed at standard personal income rates.

Related: Calculating tax on dividends: A guide & example

Company pension provision

In a limited company, you may be able to take advantage of a company pension scheme as well as investing funds in a private personal pension scheme. Sole traders have to make their own provision by joining a personal pension scheme and making regular payments.

Disadvantages of a private limited company

While a private limited company offers many important advantages, there are also a number of disadvantages.

Higher set-up costs

When you set up a private limited company, you must register your business with companies house, choose directors and shareholders, identify any people with significant control, prepare the company’s constitutional documents and complete the incorporation filing. As of 2026, standard digital incorporation costs £100 and paper incorporation costs £124. Directors and PSCs must also meet Companies House identity verification requirements and provide their Companies House personal code where required.Sole traders, in contrast, only have to register with HMRC for income tax purposes.

Greater administrative burden

Private limited companies must keep company records and accounting records, including shareholder details, shareholder votes and resolutions, share transactions, debentures, indemnities, charges and financial records. From 18 November 2025, companies no longer have to maintain local registers of directors, directors’ residential addresses, secretaries or PSCs, but they must still keep Companies House information up to date and maintain a register of shareholders.

You also have to comply with any relevant laws, rules or regulations, maintain accurate business records, file accounts and pay Corporation Tax. If the burden is too high, you may have to consider appointing a Company Secretary to handle those tasks, adding to business costs.

Related: The rise of management accounting and its importance to small businesses

Public scrutiny

Your business records held at Companies House are open to inspection by competitors, investors and other third parties. Company information filed at Companies House is publicly available, including key ownership, officer and filing information. However, the level of financial detail visible depends on the company’s size and filing regime. For example, small companies currently do not have to deliver a profit and loss account to Companies House, so turnover may not always be visible on the public register.

Financial reporting

You must maintain accurate financial records and file them with HMRC and Companies House following the end of the financial year. That means preparing statutory accounts and filing the required accounts with Companies House, as well as filing a Company Tax Return with HMRC. Depending on size, a company may be able to use micro-entity or small company filing provisions, including abridged accounts where the relevant conditions are met. For accounting periods beginning on or after 6 April 2025, a company is small if it meets at least two of these conditions: annual turnover of no more than £15 million, balance sheet total of no more than £7.5 million, and no more than 50 employees on average.

Sole traders only have to file a Self-Assessment Tax Return, giving a profit figure and a summary of income and expenditure.

We can also explain the extra filing and accounting responsibilities before you incorporate, so you know exactly what will change.

Related: Year-end accounts checklist for small businesses

Take professional advice

There are clear potential benefits in setting up a private limited company, but there are also strong disadvantages. Making a decision about the right structure for your business can be complex and must be based on sound business and financial principles.

If you are unsure whether to stay as a sole trader or set up a limited company, Accounts and Legal can help you compare both options clearly. We will look at your profits, tax position, personal income needs, risk exposure and growth plans, then explain whether incorporation is likely to benefit you.

Speak to our small business accountants for practical advice before you incorporate. We can help with company formation, tax planning, accounting setup and ongoing compliance, so you can move to a limited company with confidence.