How much can you earn before paying tax?

23 Oct 2023Whether you’re rocking the small business owner’s life or clocking in as an employee, you’ve probably had this burning question in your mind: “How much moolah can I make before HMRC comes knocking for taxes?” (How much can you earn before paying tax, in plain English).

Well, no more wondering. We’ve got your back!

We’re here to spill the beans and throw in some handy tips to help you make your money stretch a little further.

But let’s not beat around the bush…..

How much can you earn before paying tax?

In the UK, how much you can earn before paying tax is easy to explain, in most scenarios, but it can get more complex.

Let’s start with the easy bit. How much can you earn before paying tax? For most people on tax code 1257L, the answer is £12,570 a year, this is called your personal allowance.

However, there are ways you can increase your personal allowance, to get more cash tax-free! Let’s break them down.

But first, did you know under some unique circumstances you may have to start paying tax on your salary straight away? If you’re being taxed in full, this may be due to your tax code.

Read more: UK tax codes and what they mean.

However, for most people, you will have the L tax code or 1257L this is the standard tax code and the one we will be using in this blog.

How do I increase my personal allowance?

For married couples, or for individuals who are registered by their local council as blind or severely sight impaired, there are special rules in place to support you.

Marriage Allowance Transfer

The marriage allowance transfer is a great little scheme that every married couple should be taking advantage of if they’re able to. Marriage Allowance Transfer lets you transfer £1,260 of your personal allowance to your husband, wife or civil partner.

So, if you or your partner are earning below the personal allowance, the higher earner in the relationship could increase their personal allowance to reduce the overall couple’s combined tax bill.

Here’s an example.

Your income is below the £12,570 personal allowance threshold so you don’t pay tax. In this example, let’s say you earn £12,000 per annum.

Your partner’s income is £38,000 due to the UK tax brackets system, which we’ll go into later, so as a couple you pay a total tax of £5,086.

When you claim Marriage Allowance you transfer £1,260 of your Personal Allowance to your partner. Your Personal Allowance becomes £11,310, and your partner gets a ‘tax credit’ on £1,260 of their taxable income.

Now your personal allowance has fallen to £11,310, you will now start paying tax on some of your income (£138 in tax). However, due to your heroic sacrifice, your partner will now increase their personal allowance to £13,830. They will now only have to pay a tax of £4,834, making your total tax bill £4,972.

Therefore, by taking advantage of the marriage allowance you’ve earned yourself £114 practically for free. Enough for a romantic meal for 2, if you can ever decide on a place to go.

Blind Person’s Allowance

Blind person’s allowance is a bit easier to explain. Quite simply, if you are registered by your local council as blind or severely sight-impaired, you’ll be entitled to a £2,870 increase to your personal allowance making it £15,440.

Both individuals in a marriage or civil partnership can claim blind persons allowance if they both qualify.

If you’re eligible for blind person’s allowance but earn below the standard £12,570 personal allowance you can transfer your blind person’s allowance to your partner whether they qualify or not. However, your partner must be:

- Married or in a civil partnership with you

- Living with you

Although, there are some exceptions. You can still transfer your blind person’s allowance to your spouse if you aren’t living with them as long as it is because of one of the following reasons:

- illness or old age, for example, where your spouse or partner is in residential care

- Working away from home

- an armed forces posting

- being in prison

- training or education

Can I lose my personal allowance?

Short answer: Yes. The highest earners will not be entitled to a tax-free personal allowance and will pay tax on their entire income.

The reduction of your personal allowance starts when you hit £100,000. From the £100,000 mark every £2 you earn you’ll lose £1 of your personal allowance. This decrease continues until it reaches £125,140.

Once you begin to earn over £125,140 you will completely lose your personal allowance.

Additionally, as you earn more the amount of tax you pay scales up in the UK tax brackets which can get a little bit more complicated. However, we’re here to break it down for you.

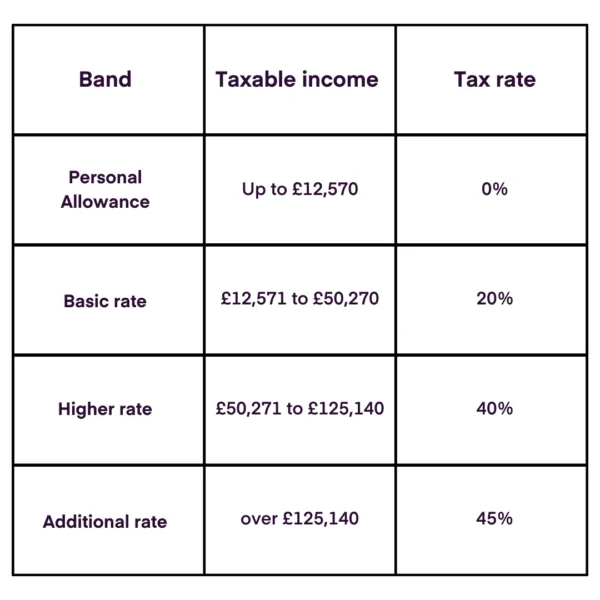

What are the UK tax brackets?

The tax bracket system scales the rates at which people pay, as you move up the brackets, you pay the different rates.

Here are all the tax brackets in the UK.

If you’re new to the UK tax bracket system you may fall for the misconception, that moving up a tax bracket means paying the new rate on your entire salary. It’s a common misunderstanding, but it’s not how the system works.

For example, if your salary went from £50,000 to £51,000 a year, your tax rate wouldn’t suddenly jump from 20% to 40% otherwise you’d just refuse the pay rise and stay on £50,000.

Instead, the tax bracket staggers as you go up in salary. So, let’s use that example again, if your salary was £51,000 you won’t pay 40% tax (£20,400).

Instead, the amount of tax you would pay over the year would work out as such:

- You’d take off your tax-free personal allowance (£51,000 – £12,570).

- Then with the remaining £38,430, £37,699 of that would be taxed at 20% (£7,539.80) as it falls in the £12,571 to £50,270 zone.

- Finally, the remaining £729 would be taxed at 40% (£291.60)

- So in total based on the UK tax brackets, with a salary of £51,000 you’d be taxed £7831.40, leaving you with £43,168.60 before other taxes and NI.

How much can you earn before paying tax if you’re a small business owner?

In the UK there’s a difference between the tax rates for base salary and dividends. Which is why we recommend a mix of the two, but why?

Well first off, salaries are subject to income tax and National Insurance contributions. As a business owner, you and your company will have to pay National Insurance on your salary, not good.

Salary payments can be used to make contributions to your pension, while dividends generally cannot. Pension contributions can be tax-efficient and help you save for retirement. Which is very good.

Second, dividends are typically subject to lower tax rates compared to salaries. There is also a tax-free dividend allowance, separate from your personal allowance. Put simply a double whammy of personal allowance, is fantastic!

However, dividend income above this allowance is subject to dividend tax rates. Therefore, we normally recommend small business owners pay themselves a small salary to first use up that sweet personal allowance.

From there we suggest you take advantage of those lower tax rates with dividend payments.

If you want to know more about paying yourself as a small business owner, contact us, and our experts can help you through the process.

Related: Dividend tax rates 2024/25: A UK guide

So, how much can you earn before paying tax?

The answer is it truly depends on your personal circumstance and what factors are in play to change it.

As a small business owner maximising your personal allowance is important for getting the most out of your salary and dividends.

If you’re looking for support with your taxes contact us, and our experts be in touch.