The Difference Between Lenders and Investors

29 May 2025For both new and established businesses, raising capital through loans or investment is a common route.

These options are popular for two key reasons: they usually offer some of the fastest and largest access to liquid cash. But just because they’re the quickest available routes doesn’t mean the process itself is fast.

Sure, you might be able to get money from your parents quicker, but unless your dad’s Bill Gates, the amount probably won’t go as far.

Securing funding is challenging. You’ll need to offer something in return, whether that’s equity in your company or proof that you can repay any debt.

So, what’s the real difference between a lender and an investor?

In short:

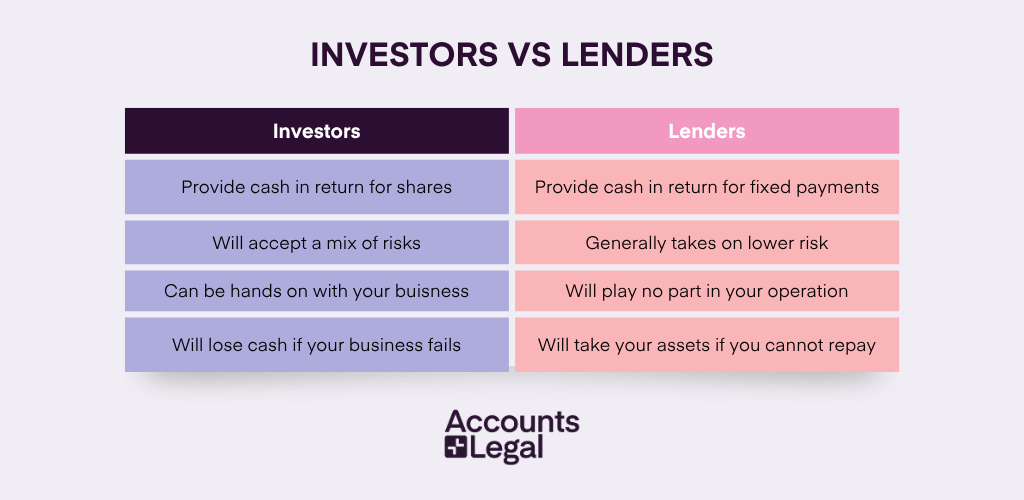

- A lender provides cash in return for regular, guaranteed repayments with interest.

- An investor gives you cash in exchange for a stake in your business, earning through dividends and, ideally, selling their share for a profit later on.

In this guide, we’ll break down the key differences between lenders and investors and explore the pros and cons of both.

What’s a Lender?

A lender is an individual or entity that provides funding, usually in the form of cash, with the expectation that you’ll repay it over time, typically with interest. The most common type of lender is a bank, offering business loans to companies and entrepreneurs.

If you’re considering a bank loan, be prepared to submit a business plan for review. Banks will assess both you and your business to determine whether it’s financially viable and capable of repaying the loan.

Business plans are used to apply for loans by showing the bank or lender what your business will be doing, how it will be making money and ultimately how you will be able to repay the debt.

Speak to our team if you need support with your business plan today.

Sole Traders and Partnerships vs. Limited Companies

Depending on whether you’re a sole trader or a limited company, the lender will want to review things differently. Here are the key differences

Sole traders & partnerships: Your personal finances will be assessed as you’ll be personally liable for the debt. Therefore, if your business can’t pay the loan back, the lender can take your personal assets.

Limited companies: The bank will want to assess the company’s repayment ability, because if the business goes bust, they won’t get their money back. Forming a limited company when requesting a loan prevents the banks from coming after your personal finances.

However, in many cases, the bank will request personal liability too. If the bank does request personal liability, whether to accept will depend on your risk tolerance. However, without personal liability, you’ll either be subject to a higher interest rate or have access to less funds.

Lenders play a huge part in the UK’s small business economy, providing vital cash in those early stages. Lenders contribute so much, that in 2023 small businesses owed around £59.2 Billion to lenders.

What’s an Investor?

An investor is an individual or entity that provides capital to a business in return for shares, which they can use to receive dividends or to turn a profit when they sell them.

Investors will seek a return on their investment, meaning you’ll have to present a strong case for your growth potential when you pitch to them.

Unlike with lenders, you’ll have a chance to negotiate your deal with an investor, as you’re selling a part of your business rather than borrowing money.

As a sole trader, you may struggle to get investment as you won’t have any shares to sell, and you’ll also be paying personal income tax on all your profits, reducing the investor’s dividends.

Therefore, as a sole trader, you should consider forming a limited company if you’re looking to seek investment.

As well as offering an instant cash injection, investors can offer you mentorship in running your business and let you access their wide network. Investors will want to see you succeed as much as you do and may inject more money if they feel it is necessary.

My thoughts on Lenders and Investors

We spoke to Neil Ormesher, CEO of Accounts and Legal, to get his thoughts on the matter. With over 25 years of experience working with clients, Neil has seen first-hand the highs and lows small businesses face when seeking loans or investments. In this section, he shares personal insights from working with clients who’ve taken on debt or partnered with investors.

When seeking cash from a lender or investor, you should be thinking medium to long term. The reason for this comes down to the high risk of failure for small businesses.

The first couple of years are always the hardest, and if you can make it through, you’ll appear as a safer bet to those willing to invest in or lend to you.

The (not so) funny thing about securing cash from a lender or investor is that when you need it most, it becomes the hardest to get. The reason for this is obvious when you think about it – businesses usually need cash during difficult periods, particularly when struggling with cash flow.

No smart lender will offer funding if they have concerns about getting their money back. Additionally, an investor won’t put money into a business they see as failing.

So, unfortunately for many small business owners, those first couple of years require you to go it alone. It’s difficult, but you can make it easier by having an accountant and business adviser from day one.

When you do reach a size that’s believed to be acceptable for investors and lenders, it’s important not to rush into securing funding. First, ask yourself: does your business really need that cash to grow? Do you have a strategic plan for how every penny will be used?

From personal experience dealing with clients, we’ve seen too many businesses take out loans without solving their cash flow issues, only to end up seeking another loan to repay the first one. Sounds bad, right? Borrowing to pay back another lender.

What’s worse is that, as we’ve mentioned, it’s hard to get cash when you desperately need it. So, our advice (and the advice any good accountant should give you) is to get your ducks in a row before applying for funding that could cause a massive amount of stress down the road.

Most lenders will also require collateral or a personal guarantee when lending to your business, putting you at risk of bankruptcy if anything goes wrong.

With all that being said, you might now feel that seeking investment is the better option. While it does carry less risk to your personal finances, there are some downsides we haven’t mentioned yet.

Most of the time, though not always, an investor will want some level of control over the business they’re investing in. If you’re a new business owner, they’ll usually ask for some say in how things are run, as the trust may not be there yet.

Even if you’re a capable owner, some investors may hesitate to go completely hands-off, especially if they’re worried you could sell your shares to someone else down the line.

The owner of the business can protect themselves from losing complete control of the business by raising something called founders shares, which are usually worth more in voting rights than any other share class. Founders may structure shares with enhanced voting rights (e.g., 2x or 3x voting per share), subject to the Articles and shareholder agreement.

On the other hand, if you’re more experienced and have a proven track record, investors may be happy to take a backseat role and receive passive income through dividends, often through alphabet shares. In some cases, you might even be able to sell a larger portion of your business without giving up control. The way to do this is through selling your alphabet shares that specifically don’t allow voting rights, and instead gives investors dividend rights.

If you’re a smaller business looking to raise investment without offering control, just know your pool of potential investors will be more limited, but not non-existent.

Here are some types of hands-off investors you could consider approaching:

Younger entrepreneurs: They often take a long-term view and are more comfortable letting the natural cycles of a business play out. They’ll typically invest in several ventures to spread their risk, expecting strong returns over time.

Retirees: Many retirees look for ways to boost their savings or generate extra income after leaving work, making them potential candidates for passive investment.

Busy investors: Some investors simply don’t have time to be involved. They’re happy to collect dividends annually without interfering in day-to-day operations.

Employees: Offering non-voting shares to employees can be a great alternative to pay rises. It gives them a stake in the business, rewards their hard work, and can increase their sense of loyalty and connection to the company.

Friends and family: If you have people close to you who want to earn a bit of extra income, but don’t necessarily know how to run a business, it can be a fantastic way to bring in some funding. Just make sure expectations are clear from the start to avoid awkward conversations later.

Investors vs Lenders: Which is right for you

When it comes to investors vs lenders, choosing the right one is entirely up to your risk levels and desire for control.

If you want to keep full control of your business and have a clear plan to repay the borrowed money, a lender (such as a bank) is the better choice.

Loans provide capital without giving away ownership, but you must repay the debt with interest, even if your business struggles. This makes loans best suited for businesses with steady cash flow and a predictable revenue stream.

On the other hand, if you need larger funding to scale quickly and are comfortable giving up a share of your business, an investor might be the right choice. Although you can look into alphabet shares if you wish to give investors a significant percentage of your business’s shares without giving up any control.

However, we find this happens rarely as most investors will want at least some say in a business their invested in. You may see investors demand more control if you’re a new and inexperienced business owner. Either way, an investor will do what they think is best for the business.

Some investors don’t expect repayments, but all expect a return on their investment, either through dividends or when the business is sold. If your business’s investor does expect repayments, this will usually be done through yearly dividends. However, you won’t be legally required to issue dividends if you’ve had a loss-making year.

No matter which route you go down, to convince both lenders and investors you’ll need a business plan. If you need support drafting your business plan, you can speak to our experts.

Meet the Author

This article has been updated and checked for accuracy as of June 2025. As CEO of Accounts and Legal, Neil Ormesher brings over 25 years of expertise in tax planning, accounting, and business strategy. A fully qualified accountant, Neil specialises in helping business owners minimise tax liabilities, optimise business structures, and navigate the complexities of tax-efficient business transactions.