Dividend Allowance 2024/25: What UK SMEs Need to Know

17 Dec 2024- £500 is the new dividend allowance for 2024/25, a significant drop from the £2000 allowance of previous years

- The basic rate on dividends over £500 is set at 8.75%, the higher rate is 33.75% and the additional rate is 39.35%.

- With this change in mind, business owners are likely to get hit with a higher tax bill and should potentially rethink their mix of salary and dividends

- There are lots of tax-efficient ways of doing this, including splitting income with a spouse, pension contributions and getting ahead of the game with an accountant (cough, cough)

- The changes come as the UK Government looks to raise funds where possible, and unfortunately in this budget, SMEs have been hit both directly, and indirectly

If you’re a business owner in the UK, you’ve probably heard about the “dividend allowance”. On the surface, it may seem complicated, but when you dig a bit deeper, you realise it really doesn’t have to be. So, before we dive into the new dividend allowance, let’s take a step back.

What is a Dividend?

If you own shares in accompany, dividends are basically a lump of money you can get paid if the company makes a profit. There used as a way to keep shareholders happy and to signal financial stability to the rest of the world, and more specifically, other investors who may want a slice of the pie in the future.

What Is the Dividend Allowance?

Think of it as your tax-free cherry on top of your dividends.

Your dividend allowance as a shareholder is the part of that sum that doesn’t get taxed by the government. It means you can earn up to that amount without having to pay tax, however what that allowance is depends on what the government sets it to at the time.

For most SME owners, this is a common way to take income from your business.

Dividends are a fairly commonplace way for business owners to take income from a business, however because of the way the dividend allowance is changed by governments, it requires a keen eye and careful planning, often with the help of a tax accountant.

Historically, it’s been a more tax-efficient than taking a salary, however the UK government has been tightening the rules on this, and 2024/25 has seen this again.

The Dividend Allowance for 2024/25

The dividend allowance has slowly been reducing over the years, here’s a breakdown of how far it has come down since 2016:

- In 2016/17 the allowance was a comparatively whopping £5,000

- By 2018/19 it was more than halved to £2,000

- 2023/24 saw it drop again to £1,000

- And 2024/25 sees it plummet to £500

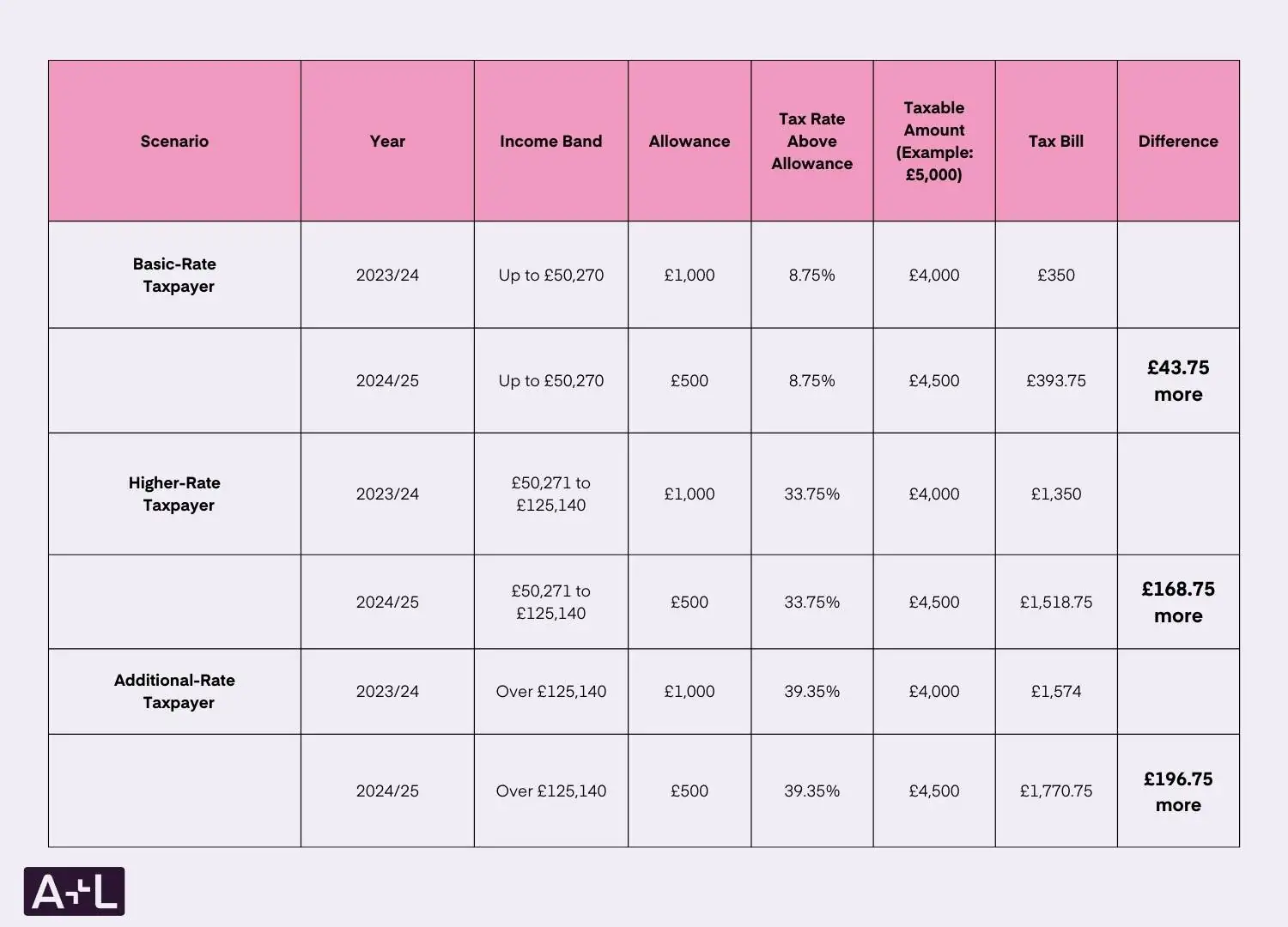

So in simple terms, for 2024/25, any dividend you receive, the first £500 is tax free, after that, it’ll be taxed at the rates below:

- 8.75% for basic-rate taxpayers

- 33.75% for higher-rate taxpayers

- 39.35% for additional-rate taxpayers

What does this mean real terms? Well, let’s use a few examples across the different tax bands.

Find out more about the dividend tax rates 2024/25 in our blog here.

How Much the Decrease in Dividend Allowance Will Affect Business Owners Tax Bill

Let’s keep it simple, let’s say in this scenario the amount of dividends being received is £5000, the workings below will give you an insight into what different tax brackets will have to pay. The UK Government is also likely to keep the tax brackets the same, which is positive news (and also makes our calculations slightly easier). So, we’ve compared it to the dividend allowance of 2023/24 which was £1000 to give an idea of how much tax bills will be going up for business owners.

What This Means for SMEs

If you’re running an SME and take dividends as part of your income, the shrinking allowance could mean a higher tax bill. In summary:

- The Allowance is Dropping: The dividend allowance reduces from £1,000 in 2023/24 to £500 in 2024/25.

- Impact Grows with Tax Band: The higher your tax band, the greater the increase in your tax bill.

- Proactive Planning: Understanding these changes helps you plan dividend withdrawals and explore potential tax-saving strategies.

This leads us nicely to how business owners can get ahead of this, and what tax strategies they can use.

Ways to Minimise Your Tax Liability

The good news is, there are things you can do as a business owner. The steps below outline some of the ways business owners can counteract the drop in dividend allowance so that you’re not giving HMRC more than your fair share.

- Reassess Your Salary and Dividends Split

The £500 dividend allowance might make it less attractive to rely heavily on dividends. Speak with your accountant (or our experts for that matter) about whether it’s time to rejig the balance between salary and dividends. - Make Use of Your Spouse’s Allowance

If you’re married or in a civil partnership, you could consider transferring shares to your spouse (if they’re in a lower tax bracket) to make use of their dividend allowance and make the most of a tax-efficient way to spread the load. - Invest in a Pension

Pension contributions can also be a tidy tax-efficient way to use your income, plus, your future-self will thank you when you’re sunning yourself in retirement. - Consider Other Allowances and Reliefs

From ISAs to capital gains tax allowances, there may be other tools at you could use to help reduce your tax liability. It’s definitely worth exploring all the options, and if that seems like a confusing task, speak to your accountant or a financial advisor. - Alphabet Shares

Also known as ABC Shares, these let you give shareholders different rights depending on their level of commitment or investment. In relation to tax, this means you can decide the level of dividend which is distributed between shareholders, which can be an opportunity to structure things in a more tax-efficient way.

- Plan Ahead with an Accountant

Finally, the best way to navigate the complexities of dividend tax is to work with a professional. A good accountant can help you plan for the long term and make sure you’re not paying more tax than necessary. (Of course, we would say that wouldn’t we?).

Why All These Changes?

So it’s clear, the dividend allowance has dropped again, just like it has done consecutively since 2016. Many people will be asking why? Well, put simply, it’s a way for the government to make money. The UK government’s Autumn Statement 2022 estimated that the lowering of dividend allowance from £2,000 in 2022/23 to £1,000 in 2023/24, and subsequently to £500 in 2024/25, is projected to generate additional revenue of approximately £1.2 billion by 2027/28.

The government is looking for ways to boost revenue, and dividends have become an easy target. It’s part of a broader effort to ensure high earners pay a fairer share of tax—but the changes inevitably hit SME owners too.

The 2024/25 dividend allowance of £500 is unlikely to be cause for celebration, but with smart planning, you can mitigate its impact. Whether it’s revisiting your pay structure or exploring other tax-efficient strategies, there are plenty of ways to adapt.

If this all feels like a lot to take in, don’t panic. At Accounts and Legal we specialise in helping SMEs navigate the ever-changing tax landscape. Give us a call or drop us an email—we’ll make sure your tax plan is as efficient as possible.