Employment Allowance: Reclaim up to £5,000

16 Aug 2023Employment allowance is a specific tax relief employers have access to, to reduce their annual National Insurance liability by up to £5,000.

A very simple, but commonly missed relief that most employer’s payroll should be taking advantage of to boost their bottom line. In this guide, we’ll run you through what employment allowance is, and how you can claim back your £5,000.

Want assistance from an expert? Contact Becky for a streamlined process.

What is Employment Allowance

Employment allowance is a reduction of your Class 1 National Insurance liability by up to £5,000 (an increase from £4,000 in 2022). For small business owners, this £5,000 can be a godsend due to the cost of employee wages usually being their largest annual expense.

Class 1 National Insurance contributions that are paid by employers are not deducted directly from their profits or personal wages. Instead, the employer’s NI contributions are calculated based on the earnings of their employees. Class 1 National Insurance are a percentage of the employee’s gross earnings and is paid on top of the employee’s wages.

As long as you’re eligible you’ll be able to save from a pot of £5,000 throughout the tax year each time you run payroll (pay your employees their wages). Once this allowance has been used, you’ll simply go back to paying normal Class 1 NI insurance until the next tax year.

Am I Eligible for Employment Allowance?

Here are the boxes you’ll need to tick to be eligible for employment allowance:

- You’ll need to be a Business or Charity, (including community amateur sports clubs).

- You must be an employer with Class 1 National Insurance liabilities under £100,000 in the previous tax year.

- Must be an entity with more than one employer PAYE reference, excluding directors.

Note: You must cover all 3 to be eligible to claim back that sweet, sweet cash.

A Few Notes

Following on from the basic eligibility there are a few more pointers you should be aware of:

- If you’re part of a group of charities or companies, the total employers’ Class 1 National Insurance liabilities for the group must be less than £100,000. If this is the case, only one company in the group can claim the allowance.

- Payments to off-payroll workers such as contractors are known as ‘deemed payments’ or IR35. You can’t include employers’ Class 1 National Insurance liabilities on deemed payments (IR35) in your calculations. Therefore, they do not count towards the £100,000 threshold.

Special Cases and De Minimis State Aid

As you may expect when it comes to claiming back from HMRC it’s not just as simple as you’d expect. For some businesses, de minimis state aid limits apply, this differs depending on which sectors you operate in.

To some companies, their employment allowance will count as de minimis state aid. De minimis state aid is capped over any 3 years.

De minimis state aid limits in most cases apply to businesses in Northern Ireland that makes or sells goods or wholesale electricity.

If this is the case, and de minimis state aid limits apply to your business, you must work out how much state aid you’ve received in total to check that you’re below the limit. You must do this even if your business does not make a profit.

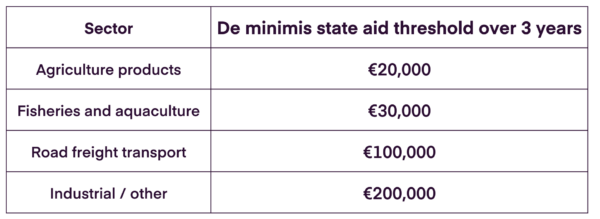

Here are the limits for the different business sectors, worked out in euros:

For assistance working out how much di minimis state aid you’ve received, you can check out the government website.

How do I Claim Employment Allowance?

So how do you get your hands on this cash, and submit a claim?

Well, first that depends on which payroll software you use, either the Governments basic PAYE tool or an alternative payroll software such as Brightpay.

You can claim through your payroll software, in the ‘Employment Allowance indicator’ field next time you send an Employment Payment Summary.

If your payroll software does not have this feature, you can use the Basic PAYE Tools.

When can I Claim?

You can claim any point within the tax year. The sooner you put your claim in the sooner you’ll receive the allowance.

Claiming for previous years

If you’ve missed a year or two, there’s no need to feel left out. With employment allowance you can claim for us up to 4 years previously, dating back to the 2018 to 2019 tax year.

The even better news is businesses under the rules of di minimis no longer apply. All you need to remember is you can only claim what the employer allowance was for those years, which goes as follows:

Employment allowance was:

- £4,000 each year between 6 April 2020 and 5 April 2022

- £3,000 each year between April 2016 and April 2020.

Final Thoughts

Getting on board the employee allowance scheme is relatively simple and a great way, especially for small businesses, to earn back a little extra cash.

If you need help with claiming employee allowance, or general payroll support, get in touch with us today.